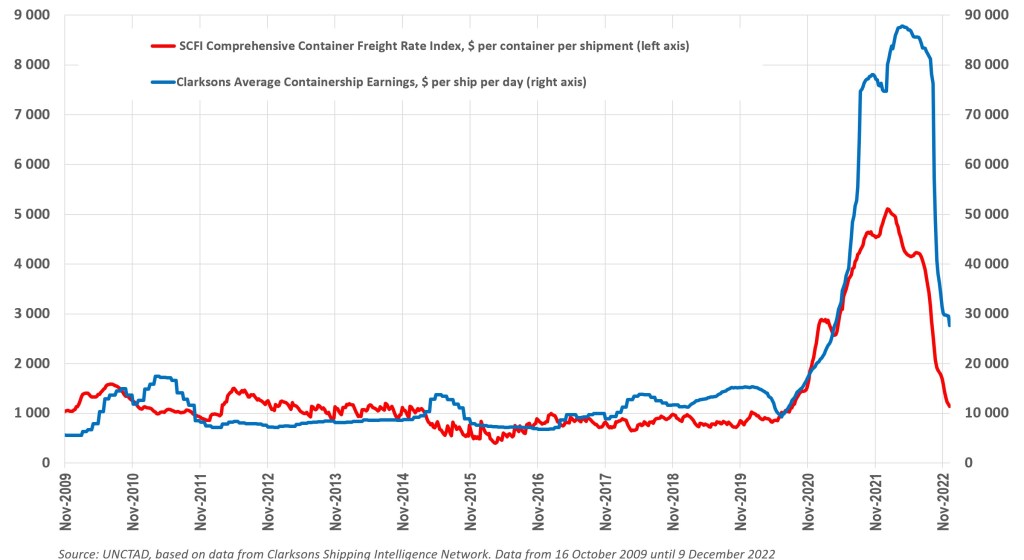

The period of 2020 to 2022 saw a historical spike in container freight rates. At its peak, the Shanghai Comprehensive Container Freight Rate Index was five times higher than the pre-covid average. Container ship earnings surged even more, to almost nine times the pre-covid average.

What happened during the supply chain crisis?

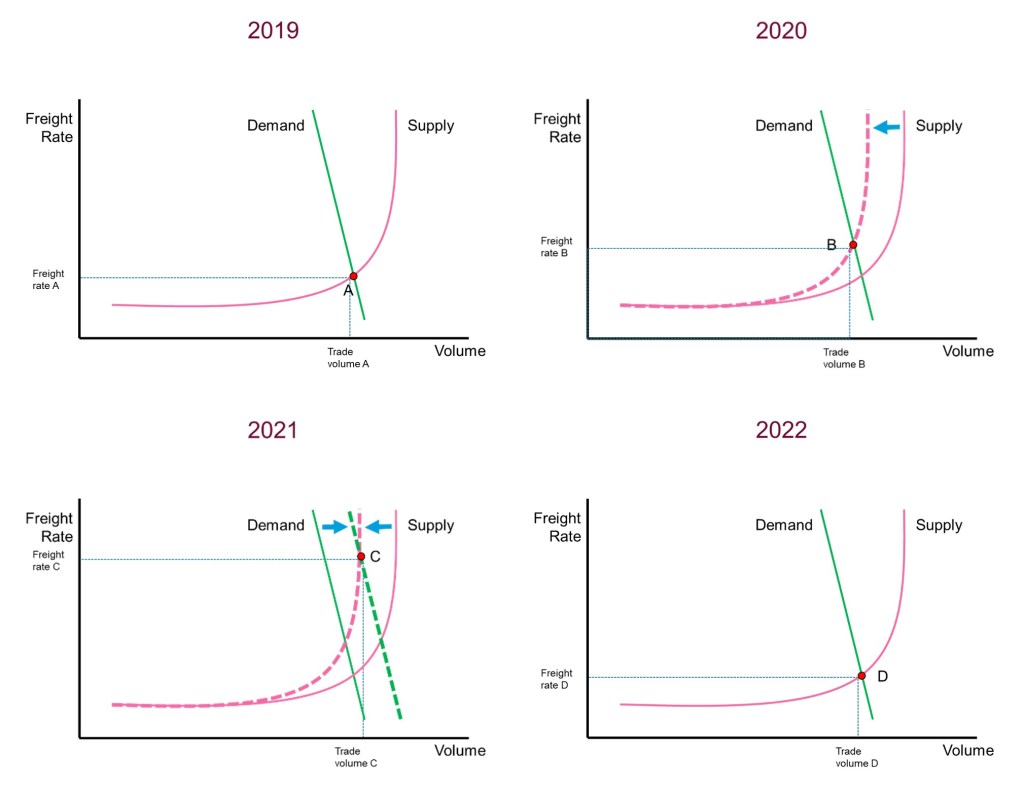

The underlying causes for this development can be illustrated in a diagram of demand- and supply-curves. The starting point is that demand for shipping services is inelastic, as transport costs are only a small portion of the final price of the traded goods; this is reflected in quite steep demand curve. The supply is elastic as long there is spare capacity, and becomes inelastic once a capacity limit is reached.

A model in three phases:

- First, in 2020: The supply curve moved to the left. The supply capacity decreased. There was little spare capacity in the market and the covid crisis caught container shipping at a moment of a historically low order book. Container ships spent about 20 per cent longer in port than pre-covid, exacerbated by supply chain blockages on land caused by covid restrictions. Schedule reliability plummeted, and available capacity was reduced by ships anchoring, waiting to be able to enter port.

- Second, mostly in 2021: The demand curve moved to the right. With economic stimulus packages, demand increased on key routes, notably out of China. Consumers reduced spending on services (restaurants, travel, movies, haircuts) and instead spent more on goods purchases (home trainers, IT gadgets, garden equipment).

- Third, since early 2022, demand and supply are moving back towards pre-covid levels. Consumers are leaving their homes and spend more of their money on services. On the supply-side, ports and transport service providers have improved operations, newly ordered ships are starting to enter the market, and port congestion is resolving. Spot freight rates on 9 December 2022 are still 18% higher than the pre-covid average, but the trend is clearly downwards.

Although there are good reasons to expect that the longer term freight rates will be somewhat higher than the pre-covid average, for the moment new container ship orders and the latest demand-supply dynamics clearly indicate that the COVID-19 induced 2020-2022 container shipping crisis is over.

Improved maritime supply chain resilience

During the pandemic, all stakeholders have invested in improving their resilience to better respond to future shocks and UNCTAD programs in trade logistics have seen a surge in demand: Port managers have been trained to improve resilience; shippers and carriers have assessed the implications of the COVID-19 pandemic for commercial contracts; port and cross border trade procedures have been reformed; a new project explores blockchain solutions for trade facilitation; Customs authorities adapted the use of Asycuda World to the Covid-19 situation; and a new comprehensive UNCTAD on-line tool helps to build maritime resilience, not just in the context of pandemics. The UNCTAD programs followed up on a 10-point plan of action published in early 2020, and benefited from a global UN project in support of transport and trade connectivity in the age of pandemics. These reforms and investments will help prepare governments and customs-, port- and maritime authorities as well as private sector operators to respond faster and more flexibly to future shocks.

Still, even with all these improvements and investments in place, freight rates will be largely shaped by the demand and supply of ships, and thus future shifts in the demand and supply curves will continue to have strong bearings on freight rates and thus global supply chains.

The far bigger challenge of the future: The energy transition and its impact on freight rates

All major shipping markets are characterized by demand- and supply-curves like those illustrated above. And in all shipping markets we have seen boom-and-bust cycles. Just during the last two years, the Baltic Dry Index surged 14-fold between May 2020 and October 2021, LNG charter rates increased 11-fold between January 2019 and December 2021, and daily oil tanker earnings increased ten-fold between July 2019 and April 2020.

Freight rate volatility is more strongly affected by shifts of the demand- and supply-curves on the horizontal axis (i.e. from left to right) than by movements along the vertical axis (i.e. fundamental changes in the cost structure).

- The supply curve may shift to the left as a result of lower speeds, port congestion, capacity management by carriers, or a fundamental under-investment in new ships, ports and intermodal transport infrastructure.

- The supply curve may shift upwards if underlying costs increase, for example due to higher fuel prices or technical measures that increase the underlying capital or operational costs for the ship owner.

These two types of shifts in the supply curve are important to understand when we look at the decarbonization of maritime transport.

The energy transition is the most important challenge the industry is facing over the next decades. Reducing GHG emissions from shipping will lead to higher maritime transport costs, be it from economic measures such as mandatory contributions per ton of CO2 emitted, or more traditional technical measures such as fuel standards and further operational efficiency targets which can only be met with more expensive ship designs and technologies. And there is no way around this. Combatting climate change is the challenge of our generation, and shipping will not be excluded. The costs of inactions would higher than the costs of reducing emissions.

However, the uncertainty about the future cost structure – including charges for CO2 emissions, alternative energies of the future, and the global regulatory framework – and the resulting delays in investments have almost certainly a stronger bearing on freight rates than the underlying changes in the cost structure. Put differently:

The shipping supply curve’s shift to the left leads to more volatility and a higher increase in freight rates than its upward move.

Three simplified scenarios for our future

Currently, investors – ship owners, energy suppliers, ports, shippers – are not sure about the future cost of emitting carbon and the global regulatory framework which may determine this. Given the great uncertainty, plus uncertainty about which low or zero CO2 emitting fuels will be available or technically viable for use on board ships or sanctioned by regulators, investors require a higher return on investment before ordering the next ship. The supply curve moves to left.[1]

An alternative scenario could include an economic measure that provides a clear and transparent picture to investors. Costs increase, which leads to an upward shift of the supply curve, but there is no underinvestment, i.e. the global capacity limit is not lowered and the supply curve does not shift to the left.

A third scenario, idealized, would lead to investments in new supply capacities, financed partly by funds generated from a global multilateral economic measure. The supply curve would move slightly upwards in line with higher basic costs, but the supply curve could – in addition – move somewhat to the right, as investments are expedited by regulations, public investments, and possibly cross-subsidies from those that still burn traditional fuels. The final freight rate may be very close to where it would be without the energy transition.

The above is a very simplified and stylized model of the impact of shifts in the supply curve in maritime transport.[2]

Of course, the exact impact of moving the demand and supply curves depends on how I draw the lines and where the curves meet at the outset. But I hope the model helps illustrate challenges and options our industry faces. The charts are intended to be a modelling framework that can support discussions on how to avoid energy transition shocks – building on lessons learned from the recent supply chain crisis in container shipping.

In conclusion

- If we have learned one thing from the 2020-2022 supply chain crunch it is that a shortage of shipping supply capacity can lead to extreme surges in freight rates, which have a strong bearing on food security, inflation, and global value chains.

- What lies ahead of us with the energy transition in maritime transport is potentially a shortage of shipping capacity in many shipping markets on numerous occasions over the next decades.

- We need to provide a stable multilateral framework – ideally via the IMO – to avoid this to happen. Both, public and private sector, need to direct funding towards sufficient investments in ports, ships, energy generation and distribution.

There is no doubt that reducing GHG emissions implies additional maritime transport costs. But: Delaying GHG reduction measures now will lead to higher costs later. And the uncertainty resulting from this delay will very likely lead to more volatility and higher increases in the freight rate (through the shift of the supply curve to the left) than the cost increases themselves.

First published on LinkedIn here: https://www.linkedin.com/pulse/end-2020-2022-supply-chain-crisis-what-we-need-learn-next-hoffmann/

[1] Note that the model of demand- and supply-curves is a static model, only comparing situations at a given point in time. It is understood that – over time – both curves will move to the right in line with a growing global economy. Thus, when I write about a “shift to the left”, this does not necessarily mean that we really have less supply than before, but we have less supply than we would have otherwise, with less uncertainty.

[2] I want to thank friends and colleagues who had kindly commented on an earlier draft of this note: Alessandro Nicita, Dominik Englert, Goran Dominioni, Georgia Spencer-Rowland, Harilaos N. Psaraftis, Hassiba Benamara, Mikael Lind, Roar Adland (Ph.D., FICS), Simon Bennett, Sotiria Lagouvardou, Voytek Chelkowski, and Wolfgang Lehmacher, as well as discussions during a recent lecture on long term trends here https://www.linkedin.com/posts/drjanhoffmann_long-term-trends-in-maritime-transport-and-activity-6998786126765293568-lwEe. The usual disclaimers apply.

Leave a comment