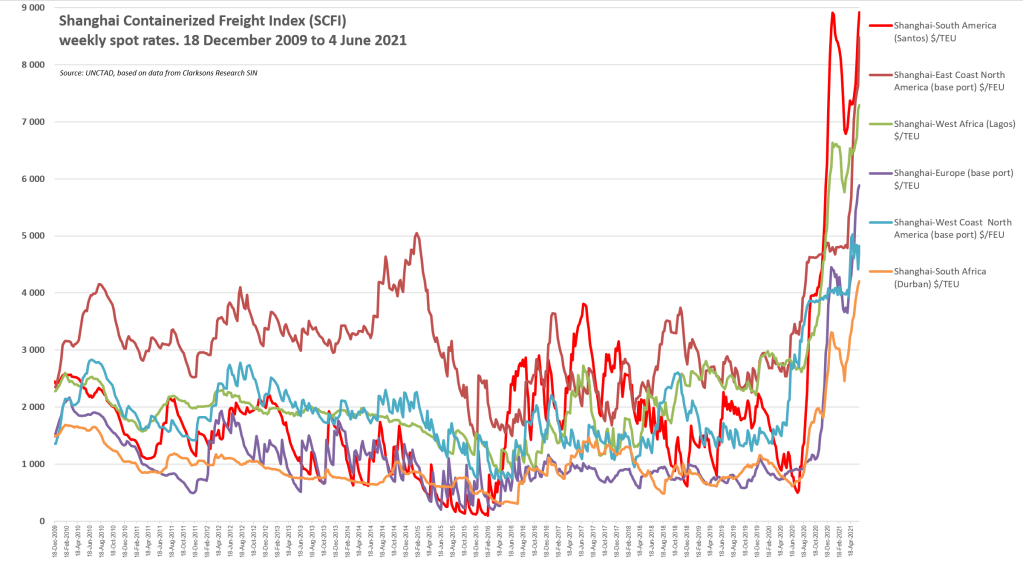

Container freight rates are reaching historical highs. And it will probably take some time for them to get back to historical averages. Thinking aloud:

1. The covid related challenges will take time to be resolved

Equipment shortages and waiting ships in Los Angeles and Yantian, on top of the earlier delays in Suez, are the immediate cause of the current high freight rates. The COVID-19 pandemic had already earlier led to containers being left in the wrong places, and still today the slow-down in ports and intermodal connections makes a container spend about 20% longer in the system. For the time being, this is not getting better but rather worse.

2. Carriers have learned not to lose out any longer

For more than a decade, liner shipping companies have confronted very low freight rates. In order to survive (except for Hanjin), unit costs needed to be reduced. To reduce unit costs, carriers invested in ever bigger (economies of scale) and newer (more fuel efficient) ships. The problem was that the older ships were not scrapped, and the overcapacity remained, or rather, got worse. Although the current order book is growing again, it takes time to build these ships. Container ships may grow a little more in size, but in my view a max TEU will be reached soon. Today’s largest container ships are of the same order of magnitude as the largest oil tankers and dry bulk carriers, which have reached their maximum several years ago. Once marginal costs are no longer below long-term average costs, the cut-throat rate war should not resume.

3. Fewer carriers than before

Linked to point 2 above, the other side of the coin, is the process of consolidation. For decades, ships got bigger, while competition and choices for shippers went down. Although carriers within the same Alliances still compete for price, the options to manage capacities and port calls has improved, from the carriers’ perspective.

4. Decarbonization of shipping: Internalizing the external costs

UNCTAD’s recent comprehensive impact assessment of the IMO short-term decarbonization measure confirmed that the measure will lead to slightly higher freight rates and slightly lower speeds. While these increases in maritime logistics costs are small when compared to the daily volatility of freight rates, they will be relevant for many years to come, until we have achieved the energy transition in shipping. Note: these cost increases do not really mean additional costs – it just means that (finally) we are moving to a situation where in future the polluter also pays, rather than only those who have so far paid the price for climate change.

5. Will the ships be built?

Trade keeps growing, while ships are slowing down. With ships waiting to unload in Los Angeles and Yantian (short-term) and going slower to reduce CO2 emissions (medium- and long-term), we will need more ships. And these ships need to be built. At the same time, confronted with an energy transition and uncertainty about in what ships to invest, ship owners may wait a little longer than usual before placing a new order. The demand/ supply balance may tilt further towards unmet demand for container carrying capacity. And as we just saw during the covid pandemic, a little shortage of containers or ships can have a high impact on freight rates.

In the very long run

Transport costs will go down. Some time in the future. Once we have managed the energy transition in maritime transport, with successfully transferring renewable “power to X”, thus reducing the marginal costs of energy per tonne-mile, shipping will become cheaper than ever before. Ships will go faster, and as a consequence we will need fewer ships for a given volume of trade. The grandchildren of today’s ship owners will find a different world of shipping. But until then, I think, freight rates will remain high for a long time.

(first published on LinkedIn here https://www.linkedin.com/pulse/5-reasons-why-freight-rates-likely-remain-high-short-jan-hoffmann)

Leave a comment